Caricatures of the Chinese real estate market fall into two camps: bears view it as a remarkable bubble that is going to burst, while bulls believe that it is part of an economic engine that has every reason to keep humming along. Bears talk about ghost cities and empty apartment complexes and costs well beyond standard income:price ratios. Bulls talk about hundreds of millions of people still in the countryside, the low quality of the existing housing stock, and the government’s desire to avoid a calamitous drop in prices. The Economist’s recent special report (which I wrote about here) on China’s urbanization touches on these debates.

First, it is important to remember the scale of the development and construction that we are talking about across China’s cities. Suzhou, a second tier city in China, is expected to have 21.5 million square feet (two million square meters) of new office space open up in the next two years, according to this Urban Land Institute report. For comparison, New York City is expected to have added nine million square feet from 2013-2015, a rate that is the fastest growth there since 1990. Suzhou is already suffering from an oversupply of empty offices:

Suzhou, about an hour’s drive west of Shanghai, is suffering from oversupply in office buildings, especially in the Suzhou Industrial Park, said the report.

The report cited an investor’s experience on a recent work visit to the Suzhou Industrial Park. “Our host joked that we were welcome to use office space in the same office building for free if we set up a company in Suzhou. There are so many empty office units in the building.”

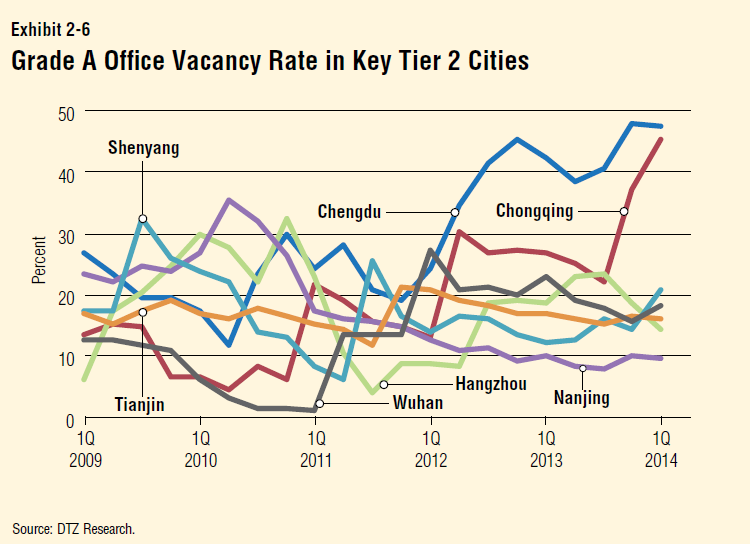

Yet despite this Suzhou is ranked #7 out of 36 large cities in real estate investment outlook by the institute. Vacancy rates in tier two cities can be staggeringly high:

How can there be any confidence that either (1) prices won’t collapse or (2) the units will remain empty? The answer is that policies–particularly related to China’s hukou (household registration) system–place significant restrictions and limits on the property market, and the prices reflect a belief in the level of demand in the absence of these limits. Restrictions still exist that make it difficult for rural born Chinese to permanently relocate to urban environments and enjoy the social service benefits of cities. Those interested in purchasing multiple units face difficulties.

Shh! As the country’s property market starts to deflate, China’s cities may be relaxing their property curbs. But it doesn’t mean they want too many people to know about it.

The latest example comes from the northeast city of Shenyang, where the glare of media attention after it was reported that the government was easing property curbs prompted some real estate types to dive for cover.

Larger Chinese cities like Shenyang are relaxing their property policies, but want to do so quietly. Officials are loath to publicize their efforts to ease curbs for fear it would seem a tacit acknowledgement that the local economy has hit the rocks.

China has managed its urbanization, spreading development around the country in order to maintain economic and especially political stability. My new book, Cities and Stability, shows how and why these actions worked.

Moving forward, however, there are real questions. The CCP leadership continues to be interested in encouraging the development of smaller cities with policy preferences and restrictions, but as the real estate sector grows in size and importance, individuals and corporations are placing billion dollar bets about the nature of these distortions and future policy changes. The property sector could absolutely slow down or indeed reverse China’s rapid GDP growth, the bedrock of economic and political confidence in the country. Biasing policies towards those born in cities while keeping out or discriminating against those born in the countryside has been a successful set of policies for the Chinese leadership for decades. Today, it encourages excess development in both lower and top tier cities. Lower tier cities focus on their recent rapid growth and upward trajectories–that are the result of policy favoritism–in attracting future investment based on extrapolation. Higher tier cities point to the restrictions that have limited growth in the recent past and encourage developers and investors to consider what would happen if the shackles came off.

Leave a comment